Table of Contents

Table of Contents

For banks, security is as much about protecting physical spaces as it is about guarding against digital threats. Branches, ATMs, cash-handling areas, and secure rooms are all targets for theft, fraud, and other criminal activity.

Without strong physical security, a single incident can lead to financial loss, operational disruption, and damaged customer trust.

See how Solink can help secure your financial services business.

10 threats to the banking industry

1. Branch robberies during operating hours

Armed robberies remain one of the most direct threats to staff and customers. They often occur during busy periods when more cash is on hand and staff are distracted. Criminals study branch layouts, staffing patterns, and routines to minimize their time on site while maximizing the haul. Even if no one is injured, the psychological impact on employees can be lasting, and public perception of safety can be damaged.

2. ATM physical attacks and tampering

ATMs are valuable targets because they combine cash access with limited human oversight. Physical attacks can involve brute force removal, explosive entry, or drilling into the cash compartment. Tampering methods include card skimmers, shimmers, and hidden cameras to capture PINs. Some attackers use “cash trapping” devices or manipulate the machine’s dispensing system to trigger multiple payouts. These attacks can occur outside regular business hours when response times are slower.

3. Cash-handling theft inside branches

The process of moving cash between tellers, vaults, and armored transport creates multiple opportunities for theft. Internal actors can manipulate transactions, skim small amounts over time, or falsify reconciliation reports. External theft can happen during cash deliveries or collections if access points are not tightly controlled. These incidents often go unnoticed for long periods if oversight relies solely on manual reconciliation.

4. After-hours break-ins

Closed branches can be attractive targets, especially in low-traffic or poorly lit areas. Criminals may target vaults, offices with sensitive information, or cash-handling equipment left on site. Entry methods range from forced doors and windows to rooftop access or bypassing alarm systems. Extended closures, such as holidays, can increase the likelihood of successful break-ins.

5. Suspicious customer behavior and pre-attack scouting

Not all threats are immediate. Criminals often conduct reconnaissance to understand a branch’s security posture. This can include loitering in lobbies, timing staff movements, testing how close they can get to restricted areas, or asking seemingly innocent questions about operations. Without staff awareness and proactive monitoring, this behavior can be dismissed as harmless until it’s too late.

6. Insider threats

Employees and contractors with legitimate access to restricted areas can abuse their position to steal cash, records, or customer data. Insider threats are not always malicious from the start; financial stress, opportunity, or coercion can change behavior over time. Because these individuals often know where security gaps exist, their actions can be difficult to detect without layered oversight.

7. Third-party and vendor exposure

Service providers—such as ATM maintenance crews, cleaning teams, or construction contractors—often need temporary access to secure areas. This opens a window for theft, unauthorized activity, or accidental compromise of security systems. Risks increase when identity checks are inconsistent or escort policies are not followed. Some attackers pose as legitimate workers to gain access.

8. Social engineering at the branch level

Criminals may impersonate inspectors, repair personnel, or corporate staff to bypass front-line defenses. In-person social engineering works because it leverages trust, urgency, and authority—especially if staff are not trained to challenge individuals in uniforms or with convincing credentials. Once inside, attackers can access cash storage, sensitive documents, or IT systems.

9. Security blind spots

Even branches with comprehensive camera systems can have areas that are poorly covered or not monitored in real time. Common blind spots include vestibules, parking lots, drive-up lanes, and areas behind counters. These gaps allow criminals to prepare or execute attacks without detection. Blind spots also make it harder to piece together a complete picture during investigations.

10. Coordinated attacks across multiple locations

Organized groups often target several branches or ATMs in a short time frame, making it difficult for individual sites to connect the dots. Without centralized monitoring, patterns of similar behavior, clothing, or vehicle use can go unnoticed. These attacks may be part of larger regional or national crime rings, and early detection often depends on recognizing trends across locations.

How Solink can help

The threats facing banks today demand more than isolated security tools—they require connected intelligence. Solink unifies your video monitoring with teller, ATM, and alarm data so every incident is captured in context. This means you can see not just what happened, but when, where, and alongside which transactions.

With Solink, you can:

Monitor every location from one dashboard – ATMs, lobbies, teller stations, vaults, and parking lots.

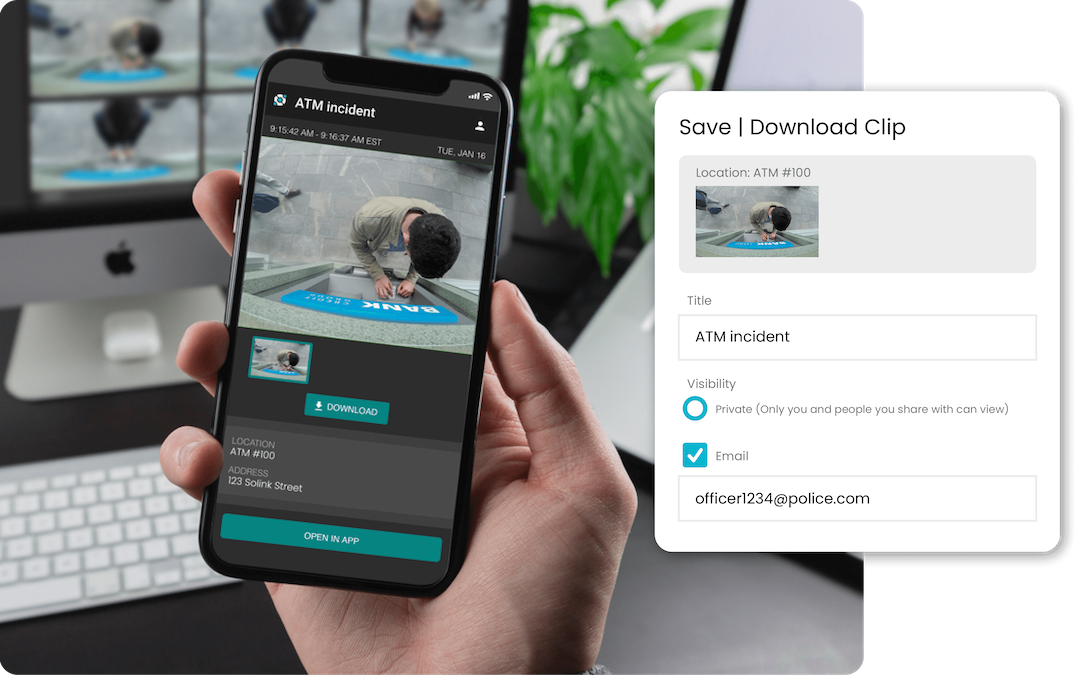

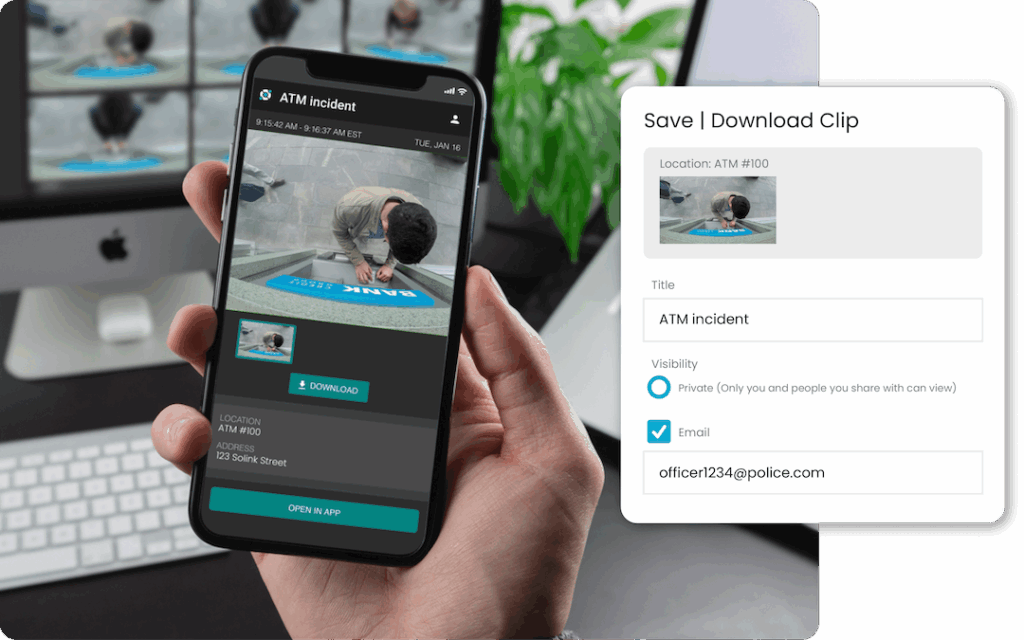

Investigate in minutes instead of hours – search by transaction, door access, or activity and instantly find matching video.

Prevent repeat losses – spot suspicious patterns across multiple branches before they escalate.

Cut false alarms – use video verification to confirm real threats and avoid unnecessary dispatches.

Stay compliant and secure – benefit from SOC 2 Type 2 protocols, customizable permissions, and complete audit trails.

Keep systems healthy – receive automatic alerts when a camera is offline or obstructed.

By aligning physical security with operational data, Solink gives your team the visibility to act faster, reduce risk, and protect both assets and people—without adding complexity to your workflow.

Using AI and video alarms for your bank

Banks need security systems that respond instantly to real threats—without wasting resources on false alarms. Solink’s Video Alarms turn your existing cameras into a smarter, faster, more reliable defense.

Fewer false alarms, faster response

By combining AI monitoring with video verification, Solink filters out nuisance triggers like animals, weather, or debris. Only probable threats are flagged for review. This means fewer false dispatches, lower fines, and an average verified police response in under nine minutes.

Smarter detection with AI

Solink’s AI doesn’t just detect motion—it understands context. It can distinguish between suspicious human activity and harmless movement, and it learns over time to refine its accuracy. The result is a security system that scales across all your branches without overwhelming your team with noise.

Cloud-based and hardware-light

There’s no need to rip and replace your existing camera system. Solink turns what you already have into a fully integrated alarm and monitoring network, managed from the cloud. This gives you a unified view of every ATM, lobby, vault, and branch from anywhere.

Verification that builds trust

When an alert is triggered, AI flags the event but humans make the final call. This blend of automation and oversight builds trust with law enforcement, so verified threats get priority response.

Deterrence before damage

Video Alarms can trigger visible deterrents—like strobes or live talkdown—before a threat moves from the outside in. This stops many incidents before they escalate.

Operational efficiency at scale

For security operations centers or teams managing multiple branches, Solink’s VerifEye console enables rapid review of hundreds of alarms with less effort. Your cameras effectively become a virtual guard network, monitoring every perimeter and key area simultaneously.

With AI-driven filtering and integrated video alarms, your bank’s security shifts from reactive to proactive—stopping threats earlier, responding faster, and protecting people, property, and assets more effectively.