Table of Contents

Table of Contents

In the 1970s, criminologist Donald R. Cressey brought together over 20 years of study to formulate what is known as the “fraud triangle.” He proposed that, for fraud to occur, especially within occupational settings, three critical factors must be present: motivation, opportunity, and rationalization. This concept has since been refined to specifically address the phenomenon of employee fraud, known as the “employee fraud triangle.”

The recent focus in the retail industry on the reduction of inventory shrinkage highlights the importance of understanding the motivations behind employee theft and fraud to effectively minimize these incidents. Some research suggests that nearly 90% of employees might engage in such activities given the right circumstances.

Therefore, simply labeling individuals who commit theft and fraud as “bad employees” fails to address the underlying issue. It’s essential to recognize these actions as stemming from employees who are sufficiently motivated, find an opportunity, and can rationalize their behavior.

What is the fraud triangle?

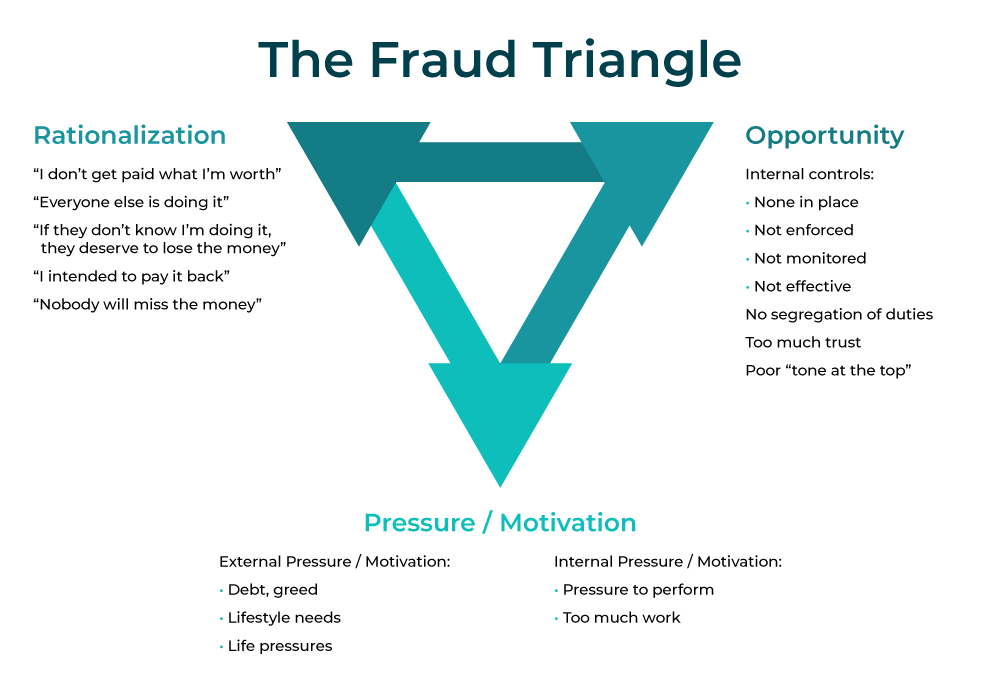

The fraud triangle diagram illustrates the trio of essential factors that prompt individuals to engage in fraudulent behavior. The following graphic delineates the fraud triangle, providing examples for each of the three critical components: opportunity, rationalization, and motivation.

Further exploration into these components reveals that, for fraud to occur:

- An opportunity must present itself.

- The individual must possess a distinct desire or necessity for committing the fraud.

- The employee must find a way to rationalize the misconduct.

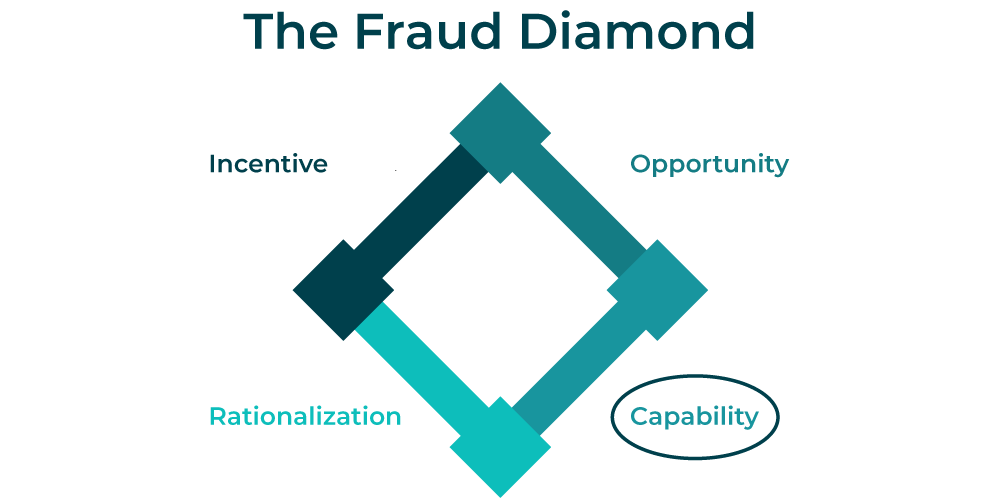

The fraud diamond: Adding the “capability” side

Alexander Schuchter and Michael Levi more recently revisited the literature on the fraud triangle, uncovering a common theme across many studies: the necessity for a fraudster to have both the “nerves and skills” for committing the crime.

Building on this idea, David T. Wolfe and Dana R. Hermanson proposed an addition to the fraud triangle, introducing “capability” as a vital fourth component. This expansion led to the concept of the fraud diamond.

Capability encompasses two primary aspects:

- Traits: There are specific personality traits, such as greed, moral weakness, overbearing pride, and dishonesty, that make it more likely someone will steal from their job.

- Abilities: Even when someone is inclined to steal from work, they need specific skills, including a deep understanding of processes and controls, a position that enables fraud, and a high level of intelligence, to successfully commit fraud (or even attempt it).

Here is a fraud diamond diagram:

Here’s a closer look at the specifics of the capability side of the employee fraud diamond.

Capability

David T. Wolfe and Dana R. Hermanson listed six main capabilities that fraudsters need:

- The individual’s role or job in the organization provides them with unique chances to find or create opportunities for fraud that others might not have.

- To engage in fraud, the person must possess the intelligence to identify and take advantage of the weaknesses in internal controls.

- Confidence or a strong sense of ego is necessary for the person to believe they can avoid detection or effectively navigate their way out of scrutiny if discovered.

- An adept fraudster is capable of persuading others to either participate in or hide their fraudulent activities.

- Being proficient in deception, a successful fraudster is not only good at lying but also prepared to do so consistently.

- High stress tolerance is a characteristic of a successful fraudster, enabling them to handle the pressure associated with their illicit actions.

Since D.R. Cressey initially formulated the fraud triangle, it has undergone various adaptations. One key adaptation highlights that the elements necessary for committing fraud also apply to the decision to commit theft.

Indeed, fraud and theft share considerable similarities, both being illegal activities where an individual takes something without consent. The distinction lies in the method: fraud involves deceit or manipulation to acquire something, whereas theft is the direct physical act of taking.

Here’s a simplified theft triangle diagram:

Here’s a simple example of how the employee theft triangle can lead a normally honest person to steal from their company:

- An employee notices there are no security cameras in their store (opportunity).

- They are having trouble paying their mortgage (motivation).

- They see their place of work as a faceless corporation that won’t miss a few hundred dollars worth of inventory (rationalization).

What is the employee fraud triangle?

The employee fraud triangle is specific to the work environment. While the basic components of the triangle don’t change, it’s important to think about the different types of employee theft separately from that of shoplifters, burglars, and other forms of external theft.

That’s because the specific motivations, opportunities, and justifications are very different.

For example, the motivation of a shoplifter could be as simple as peer pressure for youth offenders, while that of a burglar might be drug or gambling addiction. Conversely, an employee’s motivations could be more empathetic—perhaps they are facing eviction, hunger, or bankruptcy.

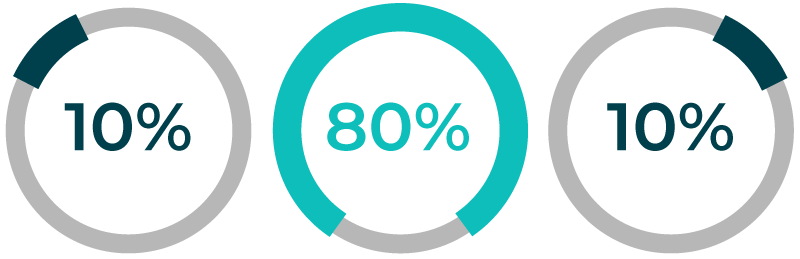

While you might feel bad for the person in such circumstances, those particulars in no way justify fraud. In this case, the best thing to do is internalize the 10-80-10 rule as a way to stop good people before they do bad things.

Why good employees fall into the triangle of fraud: the 10-80-10 rule

To effectively prevent employee theft before it occurs, it’s crucial to limit the chances for theft to take place. The 10-80-10 rule provides a helpful guideline: it suggests that 10% of employees will never engage in theft, 80% could be tempted under the right combination of opportunity, motivation, and rationalization, and 10% are actively looking for chances to commit theft.

It’s important to note, however, that this rule has faced criticism, and alternative perspectives exist. A notable example involves Paul Feldman’s experiment, famously discussed in the first “Freakonomics” book, where he sold bagels on an honor system in New York City offices. Findings showed that 87-92% of bagels were paid for, suggesting that only about 8% of people acted dishonestly, with an additional 5% displaying conditional dishonesty, and around 85% behaving honestly.

However, this scenario, which presents a more optimistic view compared to the 10-80-10 rule, involved upper-middle-class individuals interacting with a low-cost office breakfast, where the motivation and rationalization for theft were minimal.

One of the most effective strategies to deter theft is by increasing the likelihood of detection, thus discouraging most employees from attempting theft. Our article on optimal camera placement in restaurants is a valuable resource for identifying and monitoring high-risk areas.

In fact, 12 Baskets eliminated employee fraud in their business with Solink:

"We used to have products and cash go missing often. That no longer exists thanks to Solink. Initially when we installed Solink, I needed to go into the platform regularly to track down thefts. Now, I've weeded out all the dishonest people. All the new staff that come in know I have this surveillance system, so they’ll get caught if they steal from me. That’s a great deterrent."

~ Christina Liu, Operations Manager

The three sides of the fraud triangle

The fraud triangle has the following three sides:

- Opportunity: For theft to occur, an individual must identify an opportunity or a moment when stealing something becomes feasible.

- Motivation (or pressure/need): There must be a driving force or a significant reason prompting the individual to engage in theft.

- Rationalization (or justification): The person contemplating theft needs to convince themselves that their actions are justifiable on a moral ground.

Opportunity

The opportunity to commit fraud hinges on two key factors. Firstly, there must be an item of sufficient value to tempt an individual into stealing. Secondly, the person considering fraud needs to believe there’s a low risk of getting caught.

An evident lack of security camera coverage around high-value items presents a clear opportunity for fraud. However, even with cameras in place, if employees are aware that these cameras are not actively monitored, that inventory checks are sporadic, or that the camera quality is poor, they may still feel confident about not being detected.

Motivation

It’s essential to recognize that, while 80% of employees might not actively seek out opportunities to engage in wrongful acts, they could be tempted if the conditions align with the fraud triangle’s elements. Key motivational factors for these employees include:

- Unfortunate life events, such as facing eviction, a partner’s job loss, or unexpected medical expenses

- Feelings of resentment towards the company, possibly stemming from missed promotions or denied raises

- Addiction issues, including drug abuse or compulsive gambling

- Basic survival needs, like the inability to afford necessary medications or food due to high inflation

Implementing support mechanisms for employees experiencing difficult times can lessen the likelihood of them resorting to theft. Moreover, by offering such support, a company can significantly enhance its role in the employees’ lives, positively influencing their behavior and reducing the motivation for theft.

Rationalization

When an employee encounters the chance to commit fraud and feels external pressures that might drive them to do so, a vast majority, perhaps around 80%, will refrain unless they can morally justify the act to themselves. This is where rationalization comes into play.

Rationalizations typically belong to one of two categories:

- It’s not a big deal: These are beliefs that the company is large enough that the loss won’t be noticed, assumptions that such acts are widespread and thus acceptable, or viewing the theft as an insignificant expense.

- The company deserves it: These are views that the company is unfair, does not compensate adequately, or the fraudster feeling that they are entitled to more, hence considering the fraud as deserved or an unofficial part of their compensation.

These rationalizations allow individuals to justify fraud, either by believing the company can easily absorb the loss, or by feeling entitled to inflict financial damage as a form of recompense.

Addressing the belief encapsulated in the first rationalization is challenging, underscoring the importance of minimizing theft opportunities wherever possible.

Conversely, the belief in the second rationalization can be mitigated by fostering a positive and caring workplace environment, demonstrating to employees that they are valued and fairly compensated.

Steps you can take to escape the employee fraud triangle

The triangle of fraud is composed of opportunity, motivation, and justification. By addressing each of these elements individually, you can significantly decrease the likelihood of employees finding themselves entangled in this triangle of fraud. Additionally, it’s vital to consider the psychological underpinnings of the 10-80-10 rule when devising strategies to combat fraud.

Let’s delve into the implications of this rule first.

Prevention by understanding the 10-80-10 rule

Before bringing someone on board, conducting background checks is a crucial step in identifying and excluding the 10% of individuals who might actively seek opportunities to engage in dishonest behavior, such as cheating or stealing from the company.

Given that internal theft represents a significant portion of all loss, background checks serve as a valuable tool for employers. They enable the making of more informed and judicious hiring decisions, effectively reducing the risk of theft within the organization.

Remove opportunities

Removing the opportunities for employees to steal from their work is the easiest way to reduce internal theft. Here are some suggestions:

- Install a cloud-based security camera system. This acts as a powerful deterrent visible to all.

- Connect Solink to your point of sale (POS) system to review high-risk transactions.

- Adopt and enforce a zero-tolerance policy towards employee fraud. Publicize the consequences and reinforce the message through signs in areas where employees frequently visit.

- Set up an anonymous reporting mechanism for employees to report fraud without fear of retribution.

- Conduct regular and detailed inventory checks to ensure all items are accounted for.

- Arrange inventory strategically to make high-value, small items less accessible and harder to steal discreetly.

- Choose a loss prevention software solution that has all the needed features and proven ROI.

Reduce motivations

To mitigate the motivation behind employee fraud, which can stem from personal hardships or dissatisfaction at work, consider the following strategies:

- Acknowledge exemplary employees through both monetary and non-monetary rewards. Even small gestures, such as highlighting the achievements of employees during meetings, can significantly boost their sense of recognition and value within the company.

- Provide access to support services for employees facing challenges outside of work. Offering resources like mental health counseling, financial guidance, and other support programs can help employees find alternatives to addressing their problems other than resorting to fraud. Additionally, these services can diminish the likelihood of employees justifying theft on the grounds of the company being indifferent to their needs.

Prevent rationalization

Addressing the rationalization for fraud requires a multifaceted approach. Here are strategies to counteract various justifications employees might use for theft:

- Personalize the business. For franchise owners, displaying a family portrait in staff areas can remind employees that fraud affects real people, not just an impersonal entity. This helps bridge the emotional gap between employees and ownership.

- Educate on the impact of shrinkage and spoilage. Use signage to inform staff that taking products, even if they are about to expire, is considered theft and explain the reasons behind this policy. Understanding the broader implications can alter perspectives on seemingly harmless actions.

- Model integrity from the top down. Ensuring that management upholds high ethical standards sets a precedent for honesty throughout the organization. Employees are more likely to mirror the behavior they see in their leaders.

- Foster a positive and team-focused workplace. Creating an environment where employees feel valued and happy reduces the inclination to rationalize fraud. When employees take pride in their workplace, they are less likely to harm it through dishonest actions.

Solink knocks down the fraud triangle

Solink directly addresses the three sides of the fraud triangle—opportunity, motivation, and rationalization—by implementing advanced AI video analytics and proactive monitoring.

By reducing opportunities for theft, acknowledging employee contributions, and fostering a positive workplace culture, Solink helps businesses safeguard against internal theft and fraud, ensuring a secure and trustworthy environment for all.

Looking for an effective loss prevention system to drive new profit? See how Solink can help.

Timothy Ware | ![]()

![]()

Solink stands at the forefront of security solutions, excelling in loss prevention and asset protection for businesses. Our content is rich in industry expertise and crafted to provide actionable insights and innovative strategies. We empower businesses to enhance their security systems, optimize operations, and protect their assets more effectively. Discover how our advanced cloud video management system can transform your security approach.